- 24 Oct, 2023

The Difference Between No Appraisal and Traditional HELOCs: Which is Right for You?

Top 3 factors influencing your HELOC process

Homeowners, here is your most awaited guide highlighting the difference between traditional HELOC and the no appraisal HELOC.

We know that the concept of using your home’s equity through a HELOC might not be new to you. However, you might still want to gain a proper understanding of the distinction between two crucial concepts of HELOC.

In this blog, we will break down the differences between the two and give you clarity on which one is right for you.

Basics of HELOC

We would like to introduce and start with the fundamentals of HELOC before going forward with the distinction.

-

A HELOC helps you to utilize the equity you have built in your home for immediate fund requirements or home improvements, enabling you to borrow against the equity.

-

HELOC has a system of revolving credit line for a pre approved amount and this amount is approved on the basis of your credit score, debt-to-income ratio, and the equity in your home.

-

They have higher credit limits as they are secured by your collateral. The interesting part is that the interest is charged only on the amount that has been borrowed.

-

As long as you stay within your credit limit, you can borrow within the draw period. Once the draw period ends, you will no longer be able to take out the cash as the repayment will begin.

What is a draw period?

The draw period is the time when you can borrow money based on the credit limit. This activity of borrowing takes place only during the draw period.

Within this period you can make interest payments on the money you have borrowed. The draw period lasts from 5 to 10 years after the draw period comes the repayment period.

All about no appraisal Heloc approach

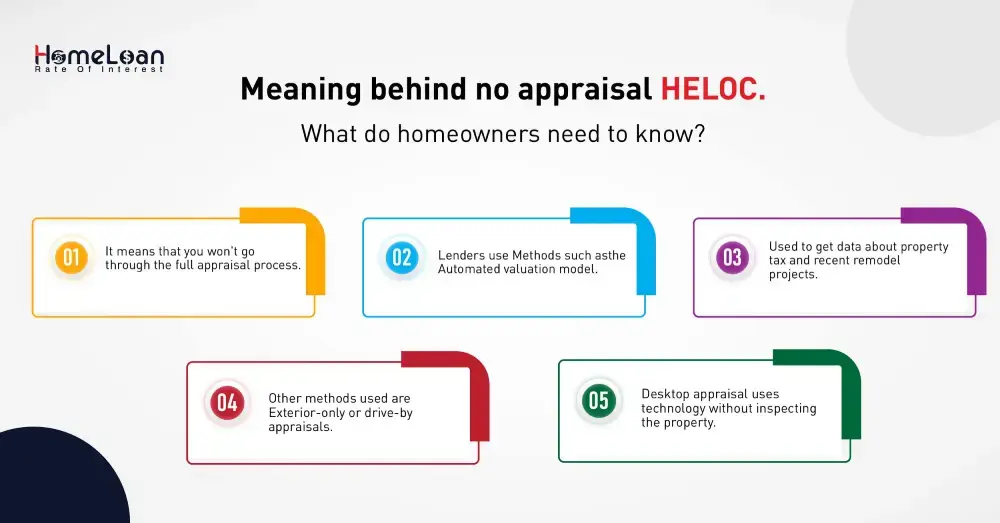

One of the most searched terms on the internet is a no appraisal HELOC. The reason is that it eliminates the need for property appraisal.

Property appraisal is the process of evaluating your property’s value before approving your requested loan amount.

After the appraisal, the professional appraiser is responsible for providing a report upon house inspection. This includes the size of your home, and its interior and exterior.

However, most individuals want to skip their appraisal process as they have immediate fund requirements. Let’s see how the HELOC without appraisal works:

-

When lenders say that they can provide HELOC without appraisal, it doesn’t mean that your home’s value won’t be determined. It just means that you will not go through a full appraisal process.

-

There are alternative methods that lenders use in order to get a fair value of your home. Methods such as the Automated valuation model (AVM) are commonly used as a replacement for a physical appraisal process to determine the home’s value.

-

It is used to obtain data about property tax assessments, home sales activity, recent home improvements, or remodeling projects.

-

Exterior-only or drive-by appraisals are also quite common; it is viewed as a combination of a full appraisal and an Automated valuation model (AVM).

-

The review from the above appraisal is matched with the data related to recent home sales in the neighborhood to get an estimation of your home’s value.

-

Lastly, there is something called a desktop appraisal where the lenders make use of technology without inspecting the property.

-

This is usually done with the help of residential real estate data and third-party inspections through interior and exterior photos.

Comparison of two types of HELOC

| The Traditional HELOC | The No Appraisal HELOC |

|---|---|

|

The application process is comprehensive and it takes some time to complete the evaluation. The lenders here assess the borrower’s creditworthiness, credit score, history, and property value. |

This particular type of HELOC is known for its speed and convenience. The application process is much faster when compared to the traditional HELOC as full appraisal is skipped here. |

| Borrowers who go through the traditional HELOC will have more flexibility in credit score requirements. | In order to balance the no appraisal factor, lenders usually have strict credit score requirements in order to process your application. |

|

One of the prime distinct factors is the appraisal of your property. A professional appraiser determines the property value in order to approve the amount of equity available for borrowing. |

As mentioned earlier, skipping the tedious appraisal process is known to save time and simplify the process. |

| The interest rates offered are competitive as they are perceived as lower risk by lenders. | Due to their speed and convenient process, no appraisal HELOCs usually have higher interest rates and certain lenders might increase it to mitigate risks. |

| Due to the appraisal process and a tedious evaluation, obtaining funds from traditional HELOC takes time. | This option is most favored by borrowers due to their quick approval process. |

Determining the right option for you

The luxury of choices often puts us in a state of confusion. We can help you choose the right option by providing adequate information, but it is not possible to decide what's best and right for you as different individuals will have different preferences and choices.

-

If you’re an individual who can afford to wait a bit longer and want to seek lower long-term interest costs, a traditional HELOC could be a good choice.

-

On the contrary, if you’re an individual who has an immediate requirement for funds, and is willing to accept a higher rate of interest, a no-appraisal HELOC could be a better option.

-

It is important to remember that the right choice is the one that perfectly aligns with your immediate financial needs, and long-term ability to handle debts.

We have certain factors that influence your decision-making in the coming section.

Drawback of HELOC without appraisal

Yes, skipping the appraisal for your HELOC is the most attractive option there is! It offers convenience and saves you time and money. But, there are some downsides to it.

-

Inaccurate property evaluation

-

Lack of full appraisal means that the lender will be using computerized methods to evaluate your property’s value. It might not be accurate due to outdated property values or estimates.

-

This may result in undervaluation or overvaluation of your property which might affect your total borrowing capacity.

-

-

Lower credit limits and Higher interest rates

-

As lenders have limited information regarding your property evaluation, they end up offering lower credit limits. This restricts your ability to borrow against your equity.

-

To top it off, they charge higher interest rates to compensate for the increased risk due to uncertain property values.

-

-

Miss out on offers

-

There are higher chances of you missing out on better HELOC offers from lenders who require appraisals.

-

A HELOC without appraisal restricts your ability to access better terms, rates of interest, and borrowing flexibility.

-

Top 3 factors influencing your HELOC process

Deciding whether you will be going ahead with a traditional HELOC or a no-appraisal HELOC lies in your hands. You need to have a clear understanding of your situation before coming to a decision.

As quoted by Dalton McGuinty - “There's no wrong time to make the right decision.”

We recommend you not depend on someone’s choices while making decisions regarding your HELOC application. Here are the top 3 factors that you need to consider to make the ideal choice.

-

Credit score

-

Your credit score is extremely important for any mortgage application. But when it comes to a traditional HELOC, there will be more leniency towards credit score requirements.

-

In addition to that, if you have a good credit score, chances are you might attract the best terms and lower interest rates.

-

Whereas no appraisal HELOCs have a bit of tight requirements when it comes to the borrower’s credit score. As the appraisal process has been skipped, the lender has no other option than to increase the interest rate.

-

-

Immediate need for funds

-

Consider your urgency. If you need quicker access to meet a financial emergency, go for an option that provides you with faster approval.

-

If you require funds to make home improvements or remodel and it is not an emergency, consider going for a traditional HELOC.

-

-

Overall ability to manage finances

-

Apart from the above two factors, we would like you to assess your complete financial strengths and weaknesses. Start with evaluating your income and expenses.

-

Consider your existing debts and pending payments. This assessment will help you understand if you can handle a HELOC. If you’re confident in your decision, go ahead and process your HELOC.

-

We agree that it is not easy to choose between the traditional and a no-appraisal HELOC. However, with awareness and understanding of the HELOC process and its requirements, we are sure you will make the right decision.

It's always a good idea to consult with a financial advisor or a mortgage professional to determine which type of HELOC is best suited to your specific needs and circumstances.

They can provide personalized advice based on your financial situation and goals.

Don’t fall into the trap of overborrowing, or getting an inaccurate loan amount due to skipped appraisal. If you’re still in a dilemma, we have HELOC related blogs where we offer strategies to help you minimize these risks.